TPD Claims for Defence Members: ADF Cover, MSBS Class A/B/C, and DVA SRDP

Defence Force TPD claims are the most operationally complex personal-insurance claims in Australia. ADF Cover, MSBS Class A/B/C, DFRDB Invalidity Benefit, and DVA Special Rate Disability Pension can all interact. Sequence matters. Here is the framework specialist advisers use.

Defence Force TPD claims are the most operationally complex personal-insurance claims in Australia. A serving or former ADF member with a permanent medical condition can find themselves navigating three separate Commonwealth regimes simultaneously — ADF Cover or MSBS or DFRDB Invalidity Benefit (depending on enlistment date), and the Department of Veterans’ Affairs Special Rate Disability Pension where the condition is service-related. Each scheme has its own definitions, its own decision-maker, and its own tax treatment. The interactions are not separately additive. Sequence matters.

This guide is for the Defence member — serving or recently separated — who is facing a TPD or Invalidity benefit claim, or who is supporting a partner or parent through one. It covers how each scheme works, where they interact, the claims-process framework we walk every Defence client through, and the line between Véurr’s financial planning in Canberra and the claims-advocacy work veterans advocates do.

It is general information, not personal advice. The financial outcomes are large, the decisions are irreversible, and the integration of scheme + tax + DVA + Centrelink is rarely intuitive — please speak to a financial adviser who has specifically advised Defence members through TPD or Invalidity claims before any election.

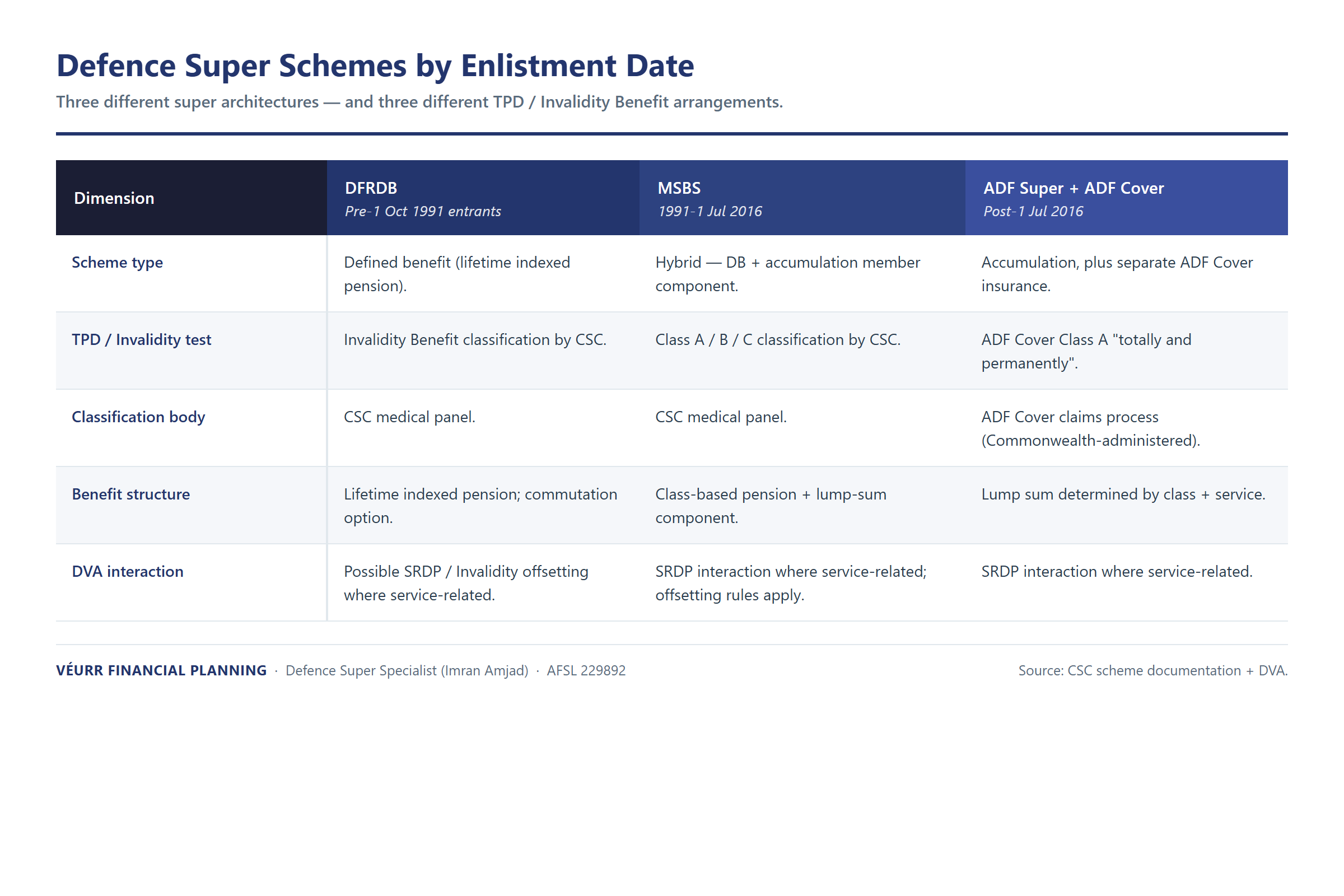

The Defence super landscape on TPD

The TPD / Invalidity arrangements a Defence member falls under depend almost entirely on the year they joined Defence.

| Enlistment date | Scheme | TPD / Invalidity arrangement |

|---|---|---|

| Before 1 October 1991 | DFRDB | Invalidity Benefit (Class A / B / C) inside the scheme |

| 1 October 1991 to 30 June 2016 | MSBS | Invalidity Benefit (Class A / B / C) inside the scheme |

| 1 July 2016 onwards | ADF Super | ADF Cover — separate Commonwealth scheme alongside ADF Super |

For a fuller treatment of how DFRDB, MSBS and ADF Super sit alongside each other — including scheme mechanics, retirement decisions, and tax treatment of ordinary retirement benefits — see our DFRDB and MSBS guide for Defence members and retirees.

This piece focuses on the TPD / Invalidity dimension of those schemes specifically — and the parallel DVA Special Rate Disability Pension (SRDP) that may apply where the condition is service-related.

Two members with similar conditions can have materially different financial outcomes depending on which scheme they fall under, whether the condition is service-related, and how the claim is sequenced. The 2016 transition split the Defence super arrangements into two architectures. The TPD / Invalidity dimension is one of the places the split matters most.

MSBS Invalidity Benefit — Class A, B, and C

For Defence members who joined between 1 October 1991 and 30 June 2016, the MSBS Invalidity Benefit is the relevant scheme pathway. The benefit is paid by the Commonwealth Superannuation Corporation (CSC) when a member is medically retired from the Australian Defence Force, and the benefit structure depends on a classification CSC determines based on medical evidence.

The three classifications:

How CSC determines classification

CSC’s classification decision is grounded in medical evidence. The process typically involves:

- The member’s medical-discharge documentation from the ADF

- One or more independent medical examinations arranged by CSC

- The member’s submission of supporting medical evidence (specialist reports, treating-doctor reports, occupational-capacity assessments)

- CSC’s medical-examiner panel review

The Class A versus Class B distinction often turns on the “reasonably qualified” test — what civil employment is the member realistically qualified for given their education, training, experience and current condition. This is where the practical-application of the legislative test gets contested. Two CSC assessments of the same member can come out differently depending on how the panel weights the residual capacity against the member’s actual qualifications.

Appeal pathway when classification feels wrong

If a member disagrees with their classification, the pathway is:

- CSC internal review. Time-limited — the request must be lodged within the prescribed period from notification. The internal review is conducted by a decision-maker not involved in the original determination, with consideration of any new medical evidence the member provides.

- Administrative Review Tribunal (ART). Where the internal review outcome is unfavourable, the member can apply to the ART (which replaced the Administrative Appeals Tribunal in late 2024 under the federal administrative review reforms). ART proceedings involve a fresh consideration of the merits, often with further medical evidence and sometimes legal representation.

- Federal Court. Limited to questions of law arising from ART decisions, not a re-hearing on the merits.

The internal review and ART pathways are formal processes. Members appealing classification typically benefit from engaging a veterans advocate or specialist legal representative — this is one of the points where the financial-planning advice and the claims-advocacy advice diverge, and we address the scope distinction further on.

ADF Cover TPD — the post-2016 architecture

For Defence members who joined from 1 July 2016 onwards, the picture is different. ADF Super (the accumulation scheme that replaced MSBS at the 2016 transition) does not contain Invalidity Benefit provisions internally. Instead, ADF Cover — a separate Commonwealth scheme administered by CSC — provides the death and invalidity benefits that sit alongside ADF Super.

ADF Cover provides:

- Class A benefits for members assessed as totally and permanently incapacitated from gainful employment, in circumstances meeting the scheme definition

- Class B benefits for members with significant but partial permanent incapacity

- Class C benefits for members discharged on medical grounds where the long-term capacity outcome remains uncertain (transitional)

- Death benefits for eligible dependants

The legislative definition of “total and permanent incapacity” used in ADF Cover differs from the “any occupation” definitions seen in retail TPD insurance. ADF Cover uses an incapacity-for-service standard, with the test applied around the member’s ability to perform the duties of their ADF role and (for the Class A finding) their likely future capacity for civilian employment given their condition.

The medical assessment process for ADF Cover claims mirrors the MSBS pattern — discharge documentation, CSC-arranged medical examinations, supporting medical evidence from the member’s own treating practitioners, and CSC panel review. The same internal review and ART appeal pathway applies.

ADF Cover benefits are paid as a combination of lump sum and pension stream depending on the classification and the member’s circumstances. The tax treatment is similar to the MSBS Invalidity Benefit pathway — the disability super benefit tax-free uplift may apply where the conditions in section 307-145 of the Income Tax Assessment Act 1997 are met, and the post-age-60 10% offset on the taxable (untaxed) element of pension components applies on the same terms as ordinary scheme retirement pensions.

DVA Special Rate Disability Pension (SRDP) — when it interacts with scheme Invalidity

For Defence members whose condition is service-related — that is, the incapacity arose from or was materially contributed to by the member’s service in the ADF — a second Commonwealth pathway opens up alongside the scheme Invalidity Benefit. This is the Department of Veterans’ Affairs.

The DVA pathway is distinct from the scheme pathway. CSC pays the scheme Invalidity Benefit under MSBS or ADF Cover (or DFRDB for pre-1991 members) based on a permanent-incapacity assessment that doesn’t itself require the incapacity to be service-related. DVA pays separate benefits under the Veterans’ Entitlements Act 1986, the Military Rehabilitation and Compensation Act 2004 (MRCA), and the Safety, Rehabilitation and Compensation (Defence-related Claims) Act 1988 (SRCA / DRCA), where the incapacity is service-related and meets the scheme’s eligibility tests.

The DVA Special Rate Disability Pension (SRDP) is one of the highest-tier DVA payments. It is offered to veterans whose service-related incapacity prevents them from being gainfully employed and who meet the SRDP eligibility criteria. Under MRCA, an eligible veteran can elect SRDP instead of MRCA permanent impairment compensation and additional income-replacement payments — the election is irreversible.

Where the offsetting bites

The interaction between SRDP and scheme Invalidity Benefit, and between SRDP and other DVA payments, involves offsetting rules that are not separately additive. The general structure:

- An MSBS or ADF Cover Class A pension (the scheme Invalidity Benefit) and a DVA SRDP are paid from different Commonwealth sources and reflect different legislative tests. Both can be paid to the same member where eligibility is established under each scheme.

- However, the assessable-income treatment of one can affect the means-tested entitlement to the other. The SRDP itself is tax-free, but the scheme Invalidity Benefit (in its taxable components) is assessable, and the combined assessable income affects any Centrelink-style income-tested supplementary benefits.

- Under MRCA, where SRDP is elected, the SRDP replaces certain other MRCA payments. The election locks in a particular tax-free income stream in lieu of other compensation forms.

- Where the member was originally entitled under the SRCA / DRCA pathway (older service-related incapacity claims), the offsetting against MRCA permanent impairment compensation is different again.

These offsetting mechanics are scheme-and-fact-specific. A member with service from 1989 (DFRDB scheme + SRCA-era service-related claim) and a member with service from 2008 (MSBS scheme + MRCA-era service-related claim) face materially different offsetting calculations even with the same medical condition.

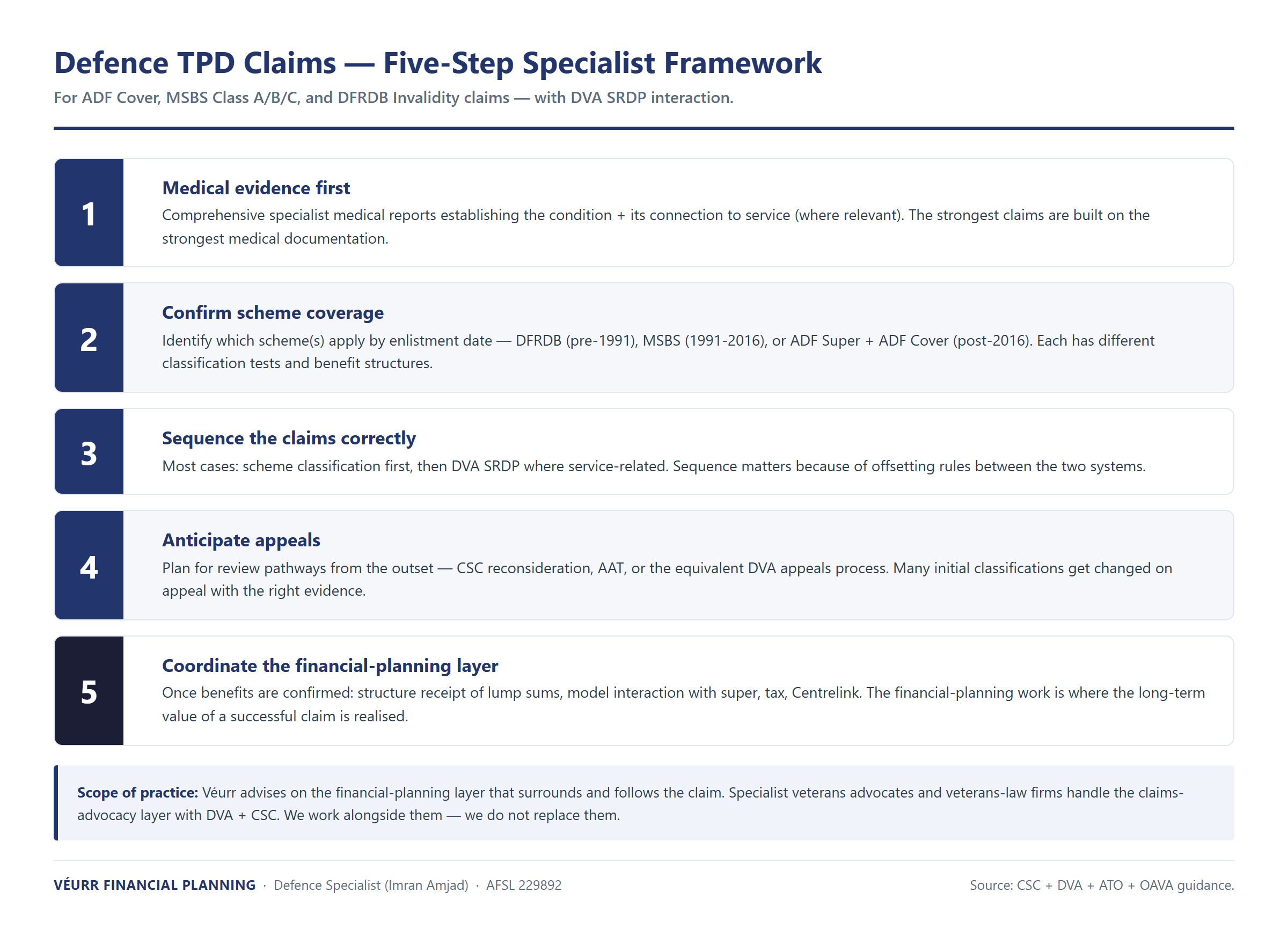

The claims-process framework specialist advisers use

There is no single “right way” to run a Defence TPD claim — the right sequence depends on the member’s enlistment date, the nature of the condition, whether it is service-related, the current employment situation, and the household financial position. Within that, there is a five-step framework specialist advisers consistently apply.

Step 1 — Medical evidence first

The single largest determinant of the claim outcome is the strength and consistency of the medical evidence. Before any claim form is lodged or any election is made:

- Treating-doctor reports documenting the condition, its history, its current functional impact, and the prognosis

- Specialist reports where the condition is in a domain requiring specialist consultation (psychiatric, musculoskeletal, neurological, oncology)

- Occupational-capacity assessments where civilian employment capacity is contested

- Records of any ADF medical events, including any DMO (Defence Medical Officer) assessments and any Defence rehabilitation programs the member participated in

- Records of any prior DVA acceptance for the condition or related conditions

A claim with weak or inconsistent medical evidence is materially harder to win, and the gap between Class A and Class B in MSBS / ADF Cover often turns on the medical evidence quality.

Step 2 — Understand which scheme(s) the member falls under

Confirm:

- The member’s enlistment date (this drives DFRDB / MSBS / ADF Cover applicability)

- Whether the member has benefit components in more than one scheme (members serving across the 1991 or 2016 transitions often do)

- Whether the condition is service-related (this is the DVA-pathway trigger)

- Whether the condition arose during a period covered by SRCA / DRCA (pre-1 July 2004 service) or MRCA (post-1 July 2004 service) — this drives which DVA legislative framework applies

This sounds clerical. It is foundational. A claim lodged under the wrong scheme assumption can take 6-12 months to correct.

Step 3 — Sequence the claims correctly

In most cases, specialist advisers run the scheme claim first (MSBS Invalidity Benefit or ADF Cover claim with CSC) and then the DVA claim, because:

- The scheme classification (Class A / B / C) is often the foundational fact that drives the DVA claim’s strategic positioning

- An SRDP election made before the scheme classification is finalised can lock in an offsetting outcome the member would not have chosen with full information

- The scheme claim timing affects the tax treatment of any lump sum (the disability super benefit calculation depends on the date of the relevant retirement event)

This is not universal. For some service-related conditions, particularly mental-health conditions with strong DVA precedent, the DVA pathway is run first because DVA acceptance can support the scheme medical assessment. The sequencing decision is one of the most consequential parts of the framework.

Step 4 — Anticipate appeals

Internal review and ART appeals are a regular part of Defence TPD claims. Plan for them at the outset:

- Document the member’s account of their condition, work history, and functional impact in writing at the earliest stage — memory fades, and consistency of evidence across multiple assessments matters

- Identify the medical specialists likely to be most influential in an ART hearing, and obtain reports from them as part of the initial submission where possible

- Budget for the time and emotional cost of appeals (12-24 months is not unusual for a contested ART matter)

- Engage a veterans advocate or specialist legal representative for the appeal — this is the claims-advocacy layer, distinct from financial planning

Step 5 — Coordinate with legal representation and engage the financial-planning layer at the right moment

Specialist veterans advocates and veterans law firms handle the claims-advocacy layer. Financial advisers handle the financial-planning layer that comes alive once the claim outcome is known. The two roles overlap occasionally but are distinct. We work with our Defence clients to ensure the financial-planning layer is engaged at the right moment in the claim — typically:

- Pre-claim: scheme-and-tax orientation, basic projection modelling, family cash-flow assessment during the claim period

- During claim: monitoring of the financial position while income is in transition (Defence-Reserve income, partner income, any interim payments)

- Post-decision: the financial-planning layer kicks in fully once the claim outcome is known and the lump sum / pension stream amounts are confirmed

Tax treatment of TPD / Invalidity benefits

The tax treatment of TPD / Invalidity benefits paid through MSBS, ADF Cover or DFRDB has three distinguishing features relative to ordinary super benefits.

The disability super benefit tax-free uplift

Where a member receives a super lump sum or pension as a result of permanent incapacity, and the disability super benefit conditions in section 307-145 ITAA 1997 are met (two medical practitioners certifying the member is unlikely to ever be able to be gainfully employed in a capacity for which they are reasonably qualified), the calculation of the tax-free component is uplifted by a formula that effectively converts more of the benefit to a tax-free component. The uplift is calculated by reference to the service period and the period from the date of incapacity to the member’s notional retirement age.

This uplift can materially change the after-tax outcome of a TPD / Invalidity lump sum, particularly for members medically retired well before age 60. A member medically retired in their 30s or 40s could see a much larger proportion of a scheme lump sum classified as tax-free under the disability super benefit calculation than under ordinary super lump sum rules.

The eligibility for the uplift turns on the medical certifications meeting the s 307-145 test — which is a stricter test than the general MSBS or ADF Cover Class A test. Not every Class A finding will automatically meet the disability super benefit tax test, and the certifications need to specifically address the “gainfully employed” and “reasonably qualified” language in the ITAA test.

Pension stream tax — under and over age 60

MSBS, ADF Cover and DFRDB Invalidity Benefit pensions are paid mostly from what tax law calls an “untaxed source” (the Commonwealth’s Consolidated Revenue Fund or equivalent). The pension-stream tax treatment follows the same pattern as ordinary scheme retirement pensions:

- Before age 60: pension is assessable income at marginal rates, similar to ordinary salary. However, where the pension is a disability superannuation income stream meeting the s 301-40 ITAA 1997 test, the 15% tax offset on the taxable component applies — materially reducing the marginal-rate exposure.

- After age 60: the taxable (taxed) component of the pension is tax-free; the taxable (untaxed) component (the bulk of a scheme Invalidity Benefit pension) remains assessable income at marginal rates but with a 10% tax offset applied.

The 15% disability superannuation income stream tax offset (pre-60) is one of the most underweighted features in DIY Defence TPD planning. It applies specifically to pensions paid because of the member’s permanent incapacity, and it does not apply to ordinary retirement pensions paid to members in similar age brackets.

Lump sum tax — different rates, different rules

Where a Class A or Class B benefit is paid in lump-sum form (subject to scheme rules), the lump sum has the standard super lump sum tax characterisation — tax-free component, taxable (taxed) component, taxable (untaxed) component — each taxed under the lump-sum rules. The disability super benefit uplift discussed above can substantially increase the tax-free component proportion where the s 307-145 test is met.

Confirm current-FY thresholds (untaxed plan cap, low-rate cap, marginal-rate brackets) with your adviser at the actual decision moment. These numbers shift annually and the tax exposure on a Defence TPD lump sum can be the largest single tax event of the member’s life.

Common DFRDB / MSBS / ADF Cover claim mistakes specialist advisers see

In our practice we see a small number of patterns recur across Defence TPD claim discussions. The patterns are not unique to any one member — they are consistent enough that we now name them when walking through the framework above.

1. Claiming DVA SRDP before scheme Invalidity classification is finalised. The SRDP election locks in a particular interaction with the scheme pathway. Members who elect SRDP before the CSC classification of Class A / B / C is finalised can find the offsetting calculation goes against them in a way they would not have chosen had they sequenced the claims differently. The right call in most cases is scheme first, DVA second — though there are exceptions (particularly mental-health conditions with strong DVA precedent).

2. Assuming “any occupation” TPD definition when the scheme uses “incapacity for service”. ADF Cover uses an incapacity-for-service standard, not the “any occupation” standard seen in retail TPD insurance. Members and their legal advisers from a retail-insurance background sometimes mis-frame the claim around the wrong test, which weakens the medical-evidence positioning.

3. Failing to pursue reclassification when the condition deteriorates. A Class B finding is not necessarily a permanent ceiling. Where a member’s condition objectively deteriorates after the initial finding, reclassification to Class A may be available through CSC review. Many Class B-classified members do not pursue this because they assume the original finding is permanent.

4. Missing the disability super benefit tax-free uplift entirely. Where a member is medically retired well before age 60, the disability super benefit tax calculation under s 307-145 ITAA 1997 can substantially increase the tax-free component of a lump sum. Members who engage a generalist accountant or tax agent who is unfamiliar with the s 307-145 test sometimes miss this entirely and pay materially more tax than they needed to.

5. Treating the scheme Invalidity Benefit and DVA pathway as separate, parallel calculations. They interact. The offsetting rules between SRDP, MRCA permanent impairment compensation, and scheme Invalidity Benefits are real and consequential. Members who treat the two pathways as if they were independent often arrive at a worse integrated outcome than they would have with coordinated advice.

6. Missing the financial-planning layer entirely after the lump sum arrives. A successful TPD / Invalidity claim often results in a substantial lump sum. The financial-planning conversation about what to do with that lump sum (super contribution strategy, investment positioning, debt clearance, family cash-flow re-engineering, Centrelink / DVA Service Pension interaction, estate planning) is where the lifetime financial outcome is largely determined. Members who navigate the claim with strong advocacy support but no financial-planning layer afterwards can end up with the same outcome regardless of the claim quality.

None of these patterns are reasons not to pursue a Defence TPD claim. They are reasons to engage the right specialists at the right moments — and to understand the difference between the claims-advocacy layer and the financial-planning layer.

When to engage a financial adviser versus a veterans-advocacy specialist

This is the scope-of-practice line. We want to be clear about what Véurr does and doesn’t do, and what other specialists do better.

Specialist veterans advocates and veterans law firms handle the claims-advocacy layer

That includes:

- DVA claim preparation, lodgement, and advocacy through the Veterans’ Review Board / ART

- MRCA / SRCA / DRCA legal interpretation and submissions

- CSC internal review and ART representation on scheme Invalidity classification disputes

- Coordination with treating practitioners on medical-evidence positioning

- Liaison with the Department of Veterans’ Affairs through the formal claims pipeline

Veterans advocates — trained through the Advocacy Training and Development Program (ATDP), with accreditation and registration now being brought under the Institute of Veterans’ Advocacy (IVA) established by the Department of Veterans’ Affairs in 2025 — and specialist veterans law firms are the right professionals for this layer. They are not financial planners, and we are not them.

Véurr advises on the financial-planning layer that surrounds and follows the claim

That includes:

- Pre-claim cash-flow modelling for the family during the claim period

- Scheme-and-tax orientation so the member and their advocate understand the financial dimension of each potential outcome

- Modelling the after-tax outcome of a Class A vs Class B vs Class C scenario at each potential election point

- Modelling the SRDP-versus-MRCA-permanent-impairment-compensation election where it arises

- Coordinating the lump sum into super (where contribution caps allow), retail investment, debt reduction, family-protection insurance, and partner-and-children planning

- Post-claim, the ongoing Centrelink / DVA Service Pension / Age Pension interaction with the new income stream and asset base

- Estate planning where the medical condition affects life expectancy

We work alongside veterans advocates and veterans law firms. We do not replace them. The two layers are distinct disciplines with distinct licensing — financial advice is regulated under the Australian Financial Services Licence framework (Véurr operates under CAR 1307015 of Lifespan Financial Planning, AFSL 229892), and claims advocacy operates under the ATDP-trained advocate framework (with accreditation moving under the Institute of Veterans’ Advocacy) and (for legal representation) law society practising certificates.

Defence members navigating a TPD / Invalidity claim are best served when both layers are engaged, in sequence, at the right moments. The framework above reflects that.

Frequently asked questions

What is the difference between MSBS Class A and Class B?

MSBS Class A is paid where the member is assessed as totally and permanently incapacitated from any civil employment for which they are reasonably qualified by education, training or experience. MSBS Class B is paid where the member has substantial residual earning capacity in some civil employment despite the permanent condition. The Class A pension is paid at a higher percentage than the Class B pension, both are CPI-indexed for life, and both can include a substantial tax-free component where the disability super benefit conditions under section 307-145 ITAA 1997 are met.

Can I claim DVA SRDP and an MSBS Invalidity pension at the same time?

Both can be payable to the same member where eligibility is established under each scheme, but they are not separately additive in all circumstances. The interaction depends on the legislative framework that applies to the service-related condition (SRCA / DRCA for pre-July-2004 service, MRCA for post-July-2004 service), the MRCA election structure where SRDP is offered in lieu of certain MRCA payments, and the means-tested treatment of the scheme Invalidity Benefit components in any supplementary income-tested payments. Integrated advice covering both pathways is essential before any election.

I was medically discharged with Class C — am I entitled to any benefit?

A Class C finding under MSBS or ADF Cover indicates that CSC has determined the conditions for a Class A or Class B Invalidity Benefit are not met — typically because the permanent-incapacity threshold is not satisfied or because the residual capacity for civil employment is judged sufficient. Class C members receive their accrued member benefit (in MSBS), their accumulation balance (in ADF Super), and any other entitlements, but not a lifetime Invalidity pension. The classification can be revisited if the member’s condition deteriorates and the permanent-incapacity test is subsequently met — which is a pathway some members underweight.

Can my Class A or Class B Invalidity pension be commuted to a lump sum?

The commutation rules for Invalidity Benefit pensions have changed over the scheme’s history and depend on the specific scheme (MSBS, DFRDB, ADF Cover). Current treatment generally restricts commutation of MSBS Class A pensions, with limited circumstances under which a partial commutation is available. The rules for DFRDB and ADF Cover differ. Always confirm the current commutation availability with CSC before electing.

Will my Defence Invalidity benefit affect my Centrelink or DVA Service Pension?

The pension stream component of a scheme Invalidity Benefit is assessable income for Centrelink and DVA means-tested payments. The lump sum component, once received, is an assessable asset (subject to deeming rules on its eventual investment form). DVA SRDP is tax-free but is included as assessable income for some other DVA means-tested payments. The integrated position needs to be modelled — the headline numbers from each scheme rarely reflect the after-Centrelink / after-DVA-Service-Pension net outcome.

I’m in ADF Super. How does ADF Cover compare to the old MSBS Invalidity arrangements?

ADF Cover provides Class A, Class B and Class C benefits in a similar architecture to MSBS, but the calculation basis is different. MSBS Invalidity Benefits are calculated from final average salary and effective service under the defined-benefit MSBS framework. ADF Cover benefits are calculated under its own scheme rules and reflect the member’s circumstances at the date of discharge. Members who served across the 2016 transition can have entitlements under both architectures depending on their service profile.

Does the disability super benefit tax uplift apply to all Defence TPD claims?

The disability super benefit uplift under s 307-145 ITAA 1997 requires two medical practitioners to certify that the member is unlikely to ever be able to be gainfully employed in a capacity for which they are reasonably qualified. This is a stricter test than the MSBS or ADF Cover Class A test, and the certifications need to specifically address the s 307-145 language. Not every successful Class A claim will automatically meet the disability super benefit test, so the medical certifications and the tax-treatment positioning are separate work-streams worth managing carefully.

Should I engage a financial adviser or a veterans advocate first?

Most Defence members benefit from both, in sequence. The veterans advocate or specialist veterans law firm should be engaged early — at the point of considering or lodging the claim — because the claims-advocacy and medical-evidence positioning is foundational. The financial adviser should be engaged in parallel for the pre-claim cash-flow and scheme-and-tax orientation, and the engagement steps up substantially post-decision when the financial-planning layer kicks in for the lump sum and ongoing income structuring. The two roles are complementary, not substitutes.

Defence TPD or Invalidity claim coming up? Get the financial-planning layer right.

Imran and Maciej at Véurr work with Defence members and their families on the financial-planning layer of TPD and Invalidity claims — pre-claim cash-flow, scheme-and-tax orientation, Class A / B / C scenario modelling, SRDP-versus-MRCA election analysis, and the post-decision lump sum and income positioning. We coordinate with veterans advocates and veterans law firms on the claims-advocacy layer.

Free 30-minute call. No obligation. No product pitch.

Or call us directly: (02) 6171 1777

Sources and further reading: CSC — MilitarySuper (MSBS) · CSC — ADF Super · CSC — ADF Cover · CSC — DFRDB · DVA — Special Rate Disability Pension · DVA — MRCA overview · ATO — Super income stream tax tables · ATO — Disability superannuation benefits · Administrative Review Tribunal