DFRDB commutation is an irreversible election with six-figure lifetime consequences. How it works, the lump-sum versus lifetime-pension trade-off, tax, and DVA layering — for Defence Force members.

DFRDB Commutation: The Irreversible Decision Defence Members Face at Separation

Most DFRDB members face one financial decision at retirement that they cannot undo. Commute, or don’t. Take the lump sum, or keep the indexed pension. The mechanics, the math, the tax, and the five-step framework before any election.

By Maciej Stanek & Imran Amjad, Véurr Financial Planning Published 23 June 2026 13 min read

Most Australian Defence Force members in the DFRDB scheme face one financial decision at retirement that they cannot undo. Commute, or don’t. Take the lump sum, or keep the indexed pension. You make this call once, it locks for the rest of your life, and once the election is paid it cannot be reversed.

This guide is for the DFRDB member — serving or recently separated — within twelve months of pension commencement, or seriously contemplating commutation in the coming years. It walks the mechanics, the math, the tax, the DVA and Centrelink interactions, and the framework we use before any commutation paperwork gets signed. It is general information, not personal advice — please speak to a financial adviser who has specifically advised DFRDB members through this decision before electing.

The DFRDB scheme in 30 seconds

DFRDB — the Defence Force Retirement and Death Benefits Scheme — is the closed defined-benefit scheme that covered Australian Defence Force members who joined before 1 October 1991, administered today by the Commonwealth Superannuation Corporation (CSC). The retirement benefit is a CPI-indexed lifetime pension calculated from rank, length of effective service, and a scheme-set multiple. It sits alongside two later schemes — MSBS (1991 to 2016) and ADF Super (2016 onwards) — but its mechanics are distinct, and the commutation election is a DFRDB-specific feature that doesn’t exist in the same form in either successor scheme. If you joined before October 1991 and earned a DFRDB benefit, the commutation question applies to you; if you joined after, you’re in MSBS or ADF Super and this framework doesn’t transfer directly.

For how DFRDB fits alongside MSBS and ADF Super — including the four-component MSBS structure and comparative tax treatment — see our DFRDB and MSBS guide for Defence members and retirees. This piece focuses on a single decision inside DFRDB: the election to commute a portion of the pension to a lump sum.

What DFRDB commutation actually is — the mechanics

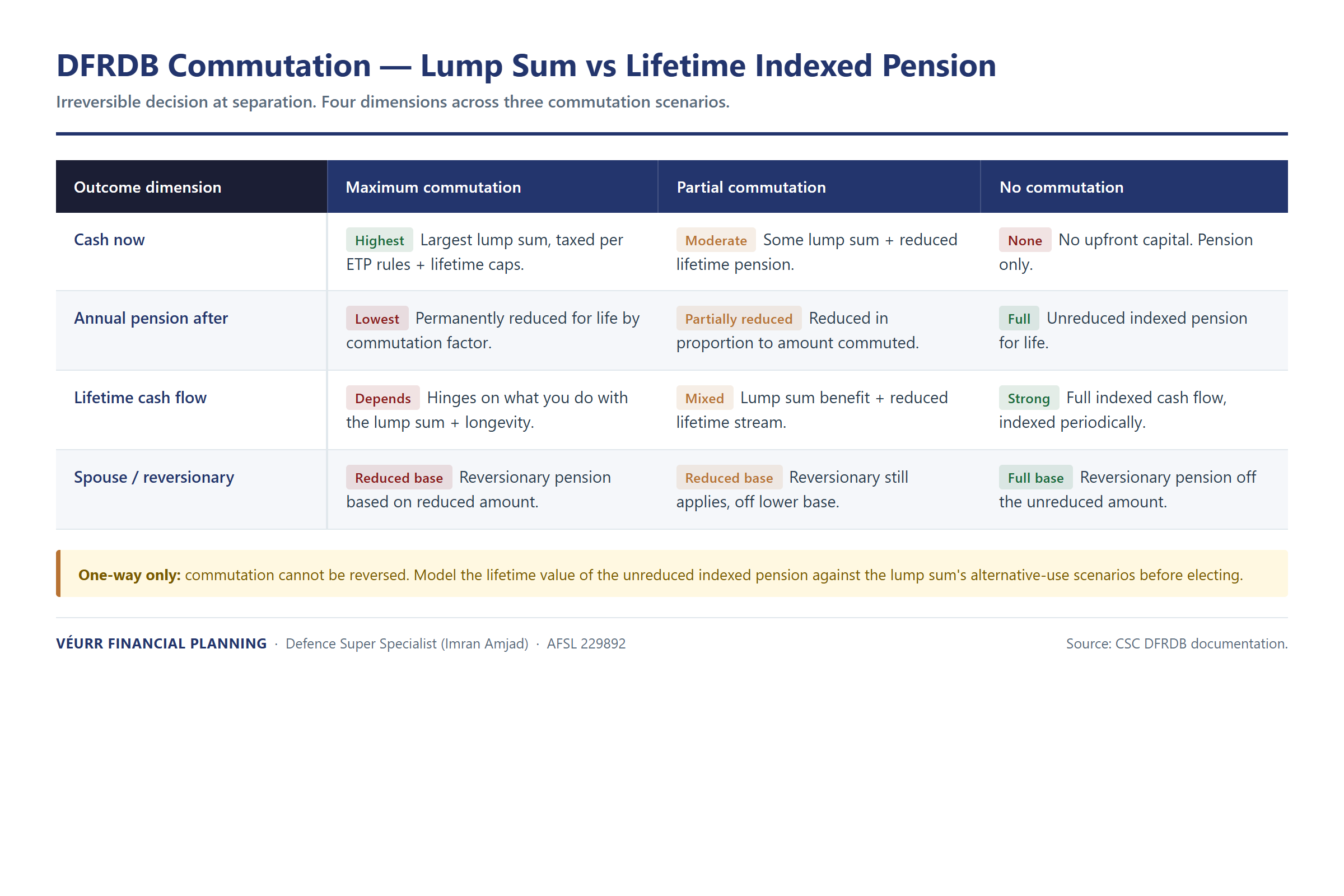

A DFRDB commutation is the scheme paying you a lump sum at retirement in exchange for a permanent reduction in your annual indexed pension. The maximum is five times your annual retirement pay, a cap that has applied from 29 June 2002 (pre-2002 arrangements used a different structure). The lump sum is divided by your life-expectancy factor at the age of election, and that quotient is the annual amount by which the pension is reduced for life. The election is made once, at separation or pension commencement; it isn’t available in service, isn’t generally available after the pension has commenced (narrow exceptions aside), and once the lump sum is paid the reduction cannot be reversed. Critically, the pension does not revert to its unreduced level even if you outlive the life-expectancy factor used in the calculation.

The life-expectancy factor in plain English. The scheme uses a published table of factors at each retirement age. Critically, those factors are not a current estimate of how long you will live — they are fixed divisors derived from the 1960–62 Australian Life Tables, and average life expectancy has risen by more than a decade since. The commutation lump sum, divided by this factor, equals the annual amount by which the pension is reduced. Because the factor is based on decades-old longevity, most members today outlive it — and the pension is never restored when they do. This was the central finding of the Commonwealth Ombudsman’s investigation: the “break-even” age implied by the factor sits well before the age most members actually reach, so a long-lived retiree keeps paying the reduction for years beyond the point at which the lump sum was, on the scheme’s own arithmetic, already repaid.

That permanent-reduction point is the one DFRDB members most commonly underweight. The most contentious feature of the regime — that the reduction continues indefinitely if you outlive the factor — was investigated in detail by the Commonwealth Ombudsman, whose findings noted that many members did not fully understand it at the time of election.

Why “irreversible” matters

Irreversibility is the defining feature of the DFRDB commutation regime, and the reason it sits in a different category from almost every other retirement-stage decision a Defence member makes. Three mechanics drive this. First, the election is single-shot, made at separation or pension commencement — no trial period, no annual review window to reconsider it. Second, the pension reduction continues for life even where the member outlives the life-expectancy factor, so a long-lived retiree keeps paying it every year past the point where the lump sum has been actuarially repaid. Third, the spouse’s reversionary pension is calculated from the member’s pension at death — the reduced pension after commutation — so the irreversibility extends past the member’s own lifetime.

DFRDB commutation: the lump-sum versus lifetime-pension trade-off, across maximum, partial and no commutation.

A common pattern: a member commutes the maximum to pay down a mortgage, then lives twenty-five years in retirement and watches the reduced pension index lower year-over-year against the no-commutation counterfactual. The cumulative gap, over that retirement plus a spouse’s reversionary period, often exceeds the original lump sum by a meaningful margin. That’s not an argument against commutation in every case — it’s an argument for modelling the decision properly before electing.

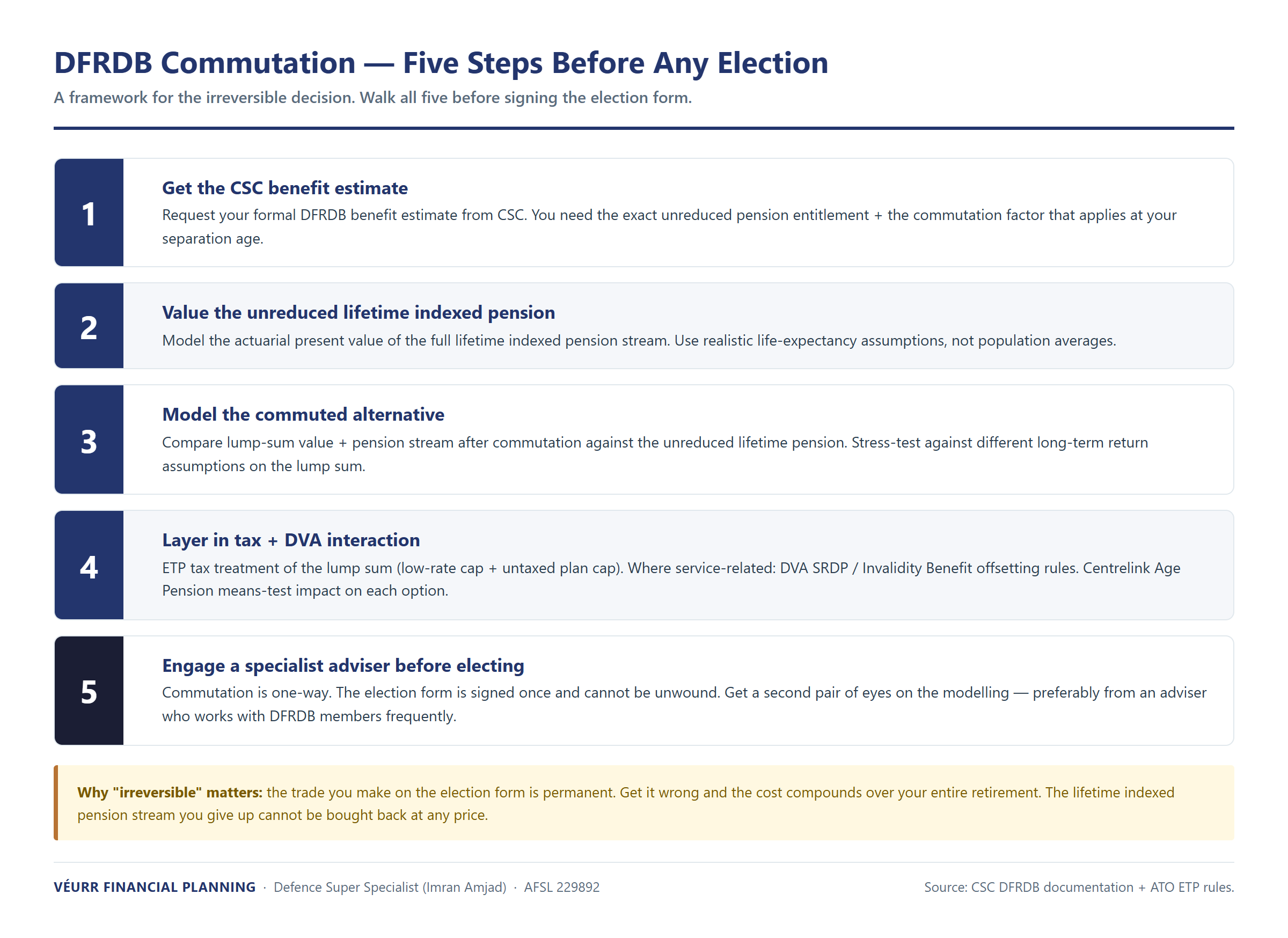

The decision framework — five steps before any election

Our five-step framework is the structured modelling pass we run with every Defence client before any election paperwork is signed. Step 1 — Get the current CSC benefit estimate so every later number sits on a defensible source document: annual retirement pay, the maximum commutation amount, the life-expectancy factor at your planned election age, and the resulting reduced pension. Step 2 — Model the lifetime value of the unreduced indexed pension over your projected longevity, using realistic assumptions (your actual health, family history and lifestyle — a member with strong family longevity should model to 90–95, not the scheme’s outdated 1960–62-based factor), and include the spouse’s reversionary tail, which for a couple in their early 60s often adds ten to fifteen years of cash flow. Step 3 — Compare to the commuted alternative: full retirement pay versus maximum commutation with the lump sum invested at a defensible expected real return (typically 3–5% above CPI for a balanced retirement portfolio), and run partial commutation as a third scenario — often the answer that best balances a cash-now use case against the lifetime value of the indexed stream. Step 4 — Layer in tax, DVA Service Pension or Centrelink Age Pension, and estate planning (the section below) — these often flip the answer Step 3 suggested. Step 5 — Engage an adviser with specific DFRDB commutation experience, because the scheme-specific factors don’t transfer from private super.

The five-step DFRDB commutation decision framework.

For Step 5, verify the adviser is listed on the ASIC Financial Advisers Register, has specifically advised DFRDB members through commutation in the last three years, and will model no-commutation, maximum-commutation, at least one partial-commutation scenario, and the reversionary implications for your spouse.

Tax treatment of DFRDB commutation

DFRDB pensions and the commutation lump sum are paid from what tax law calls an “untaxed source” — practically, the Government’s Consolidated Revenue Fund — and that characterisation drives the after-tax math. The pension stream is fully assessable at marginal rates pre-age-60. From age 60 the taxable (taxed) component becomes tax-free, and the taxable (untaxed) component, which is the bulk of a DFRDB pension, attracts a 10% offset on the untaxed element while remaining assessable income (the offset materially improves the after-tax pension at 60 even though the gross pension doesn’t change). The commutation lump sum is treated as a superannuation lump sum, with tax-free, taxable (taxed) and taxable (untaxed) components in the same proportions as the underlying benefit (calculated by CSC and disclosed in the benefit estimate). The untaxed component is taxed at concessional rates up to the untaxed plan cap and top marginal rates above — for a senior officer commuting near the maximum, that’s often the single largest tax exposure of the retirement.

The tax rates that apply to each component of the lump sum depend on the member’s age, the size of the lump sum, and current ATO thresholds:

Component

Pre age 60

Post age 60

Tax-free

Tax-free

Tax-free

Taxable (taxed)

Concessional rates up to low-rate cap; top marginal above

Tax-free

Taxable (untaxed)

Concessional rates up to untaxed plan cap; top marginal above

Concessional rates up to untaxed plan cap; top marginal above

That’s why getting the lump-sum size right, watching the untaxed plan cap, and timing the commutation around other income events in the financial year all matter.

Important: Confirm the current-FY thresholds (low-rate cap, untaxed plan cap, marginal-rate brackets) with your adviser at the actual decision moment. These numbers shift annually and the after-tax outcome of a DFRDB commutation is highly sensitive to which thresholds apply.

DVA Special Rate (TPI) and Invalidity Benefit interaction

For DFRDB members whose benefit involves an Invalidity Benefit classification, the commutation decision sits at the intersection of three regimes: the DFRDB benefit itself, the DVA Service Pension for veterans with qualifying service, and the DVA Special Rate Disability Pension (commonly called “TPI”) for veterans whose service-related incapacity prevents gainful employment. The interactions are not additive: the Special Rate Disability Pension in particular has offsetting rules where it operates alongside a DFRDB Invalidity Benefit — the two streams aren’t separately payable in full in all circumstances, and the sequence of elections matters. An Invalidity-classified member needs integrated modelling running the three regimes together, not as separate calculations. The wrong sequence can cost meaningful lifetime value, and the irreversibility of the DFRDB election means it can’t be unwound after the lump sum is paid.

Centrelink Age Pension interaction

For DFRDB members without qualifying service for DVA, the Centrelink Age Pension is the income-support pathway, and commutation interacts with it in two opposing ways. On the assets-test side, a commuted lump sum becomes an assessable asset once received (subject to the deeming rules on whatever form it takes) and can push the household above the threshold depending on size and other holdings. On the income-test side, a reduced DFRDB pension lowers assessable income versus the unreduced pension, and the net position can move either way depending on how the lump sum is invested. The after-Centrelink position can differ from the headline pension reduction by a meaningful margin — which is why modelling Centrelink alongside the DFRDB cash flow is core to the framework above.

Common DFRDB commutation mistakes specialist advisers see

Five patterns recur across DFRDB commutation decisions in our practice, consistent enough that we now name them explicitly when working through the framework. (1) Over-commuting — the lump sum feels proportionate to a near-term cash use case (mortgage payoff, renovation, helping adult children) while the lifetime value of the foregone pension stream gets underweighted. (2) Underestimating longevity — the scheme’s life-expectancy factor is built on the 1960–62 life tables and understates today’s longevity by more than a decade, so members with strong family longevity, a good health profile and a non-physical post-Defence career routinely outlive it — and the pension is never restored when they do. (3) Failing to model the spouse’s reversionary stream — the most under-modelled element, calculated from the reduced pension and able to run fifteen to twenty years past the member’s death where the spouse is materially younger. (4) Ignoring the post-age-60 inflection — sizing the commutation on pre-60 tax rates and forgetting the 10% offset improves the after-tax pension from 60. (5) Treating the commutation in isolation from DVA Service Pension or Centrelink eligibility — the integrated position can flip the answer. None of these are reasons to never commute; they are reasons to model the decision properly, with someone who has scheme-specific experience, before any election.

Frequently asked questions

Is DFRDB commutation always irreversible?

Once a DFRDB commutation election is paid, the resulting pension reduction is permanent. A member cannot subsequently elect to repay the lump sum and restore the original pension. There are narrow scheme circumstances under which an unpaid commutation election can be withdrawn before the lump sum is paid, but once payment has occurred the election locks. The pension reduction continues for the remainder of the member’s life, even if the member outlives the life-expectancy factor used in the original calculation.

Can I commute a portion only, rather than the full maximum?

Yes. A DFRDB member can elect to commute any amount up to the maximum, which is five times annual retirement pay (applicable from 29 June 2002 onwards). Partial commutation is often the right answer for members who have a specific use case for a smaller lump sum, such as mortgage payoff or debt clearance, but want to preserve the bulk of the indexed pension stream. The same five-step decision-framework modelling applies equally to partial-commutation scenarios.

How does commutation affect my spouse’s reversionary pension?

The reversionary pension paid to an eligible spouse on the member’s death is calculated as a percentage of the member’s pension at the date of death. After commutation, the member’s pension is the reduced pension, so the reversionary stream is correspondingly lower. This is one of the most consequential aspects of the commutation decision for members with a spouse, particularly where the spouse is materially younger than the member and would be expected to receive the reversionary pension for many years past the member’s death.

I’m in receipt of a DFRDB Invalidity Benefit. Can I commute?

DFRDB members on an Invalidity Benefit pension have access to commutation under the scheme rules, but the interaction with the Invalidity Benefit classification (Class A, B, or C), the tax treatment of an invalidity-class benefit, and any DVA pathways including Service Pension and Special Rate Disability Pension is materially more complex than for ordinary retirement commutation. Members in this position should obtain integrated advice covering the DFRDB, DVA and tax dimensions together before any election is made.

Can I commute now and re-think the decision in 12 months if my circumstances change?

No. Once the commutation lump sum is paid, the pension reduction is permanent and cannot be undone. The pre-election period is the only window in which the decision is reconsiderable. This is why a structured modelling pass at least 12 months before the planned election date is so important. There is no trial period, no annual review, and no scheme-level mechanism to reverse a paid commutation.

Do I pay tax on my DFRDB pension after 60?

Often, yes. Unlike most super pensions, a DFRDB pension does not automatically become tax-free at 60: the taxed element becomes tax-free, but the untaxed element — which typically makes up the bulk of a DFRDB pension — remains assessable at your marginal tax rate with a 10% tax offset on the untaxed element, and that offset is subject to an annual cap. In practice the offset materially improves the after-tax pension from age 60 even though the gross pension does not change. The exact split between your taxed and untaxed elements is set out in CSC benefit information, and it is worth confirming before making decisions that hinge on the after-60 position.

Does DFRDB affect the Age Pension?

Yes — mainly through the income test. A DFRDB pension is a defined-benefit income stream: Centrelink assesses the gross pension less any deductible (tax-free) amount, and unlike civilian defined-benefit pensions, the usual 10% cap on that deductible amount does not apply to military defined-benefit income streams. The pension itself does not count in the assets test, but a commuted lump sum becomes an assessable asset once received, with deeming applied to whatever financial form it takes. The net Age Pension position can move either way after commutation, which is why modelling Centrelink alongside the DFRDB cash flow is part of the framework above.

DFRDB commutation decision coming up? Get it right first time.

Imran and Maciej at Véurr work with DFRDB members on the commutation election, the lifetime-value modelling, the DVA and Centrelink interaction, and reversionary planning. Once made, the decision is irreversible — get specialist advice before you elect.

Free 45-60 minute Initial Meeting. No obligation. No product pitch.

Imran Amjad is a financial adviser at Véurr Financial Planning (ASIC Authorised Representative No. 000321135), specialising in Defence and Commonwealth super, retirement-stage advice for ADF members and veterans, and integrated planning across DFRDB, MSBS, ADF Super and the DVA pathways. Verify Imran’s authorisation on the ASIC Financial Advisers Register.

Maciej Stanek is the founder and senior financial adviser of Véurr Financial Planning (ASIC Authorised Representative No. 000449178), with more than 20 years experience in the finance industry advising Commonwealth and Defence super members on retirement, commutation, and complex transition decisions. Verify Maciej’s authorisation on the ASIC Financial Advisers Register.

Véurr Financial Planning Pty Ltd (ABN 16 635 751 423) is a Corporate Authorised Representative (No. 1307015) of Lifespan Financial Planning Pty Ltd (ABN 23 065 921 735, AFSL 229892).

General advice warning: This article is general information only and does not constitute personal financial advice. It does not take into account your personal objectives, financial situation, or needs. Before acting on any of the information in this article, you should consider whether the information is appropriate for you in light of your circumstances, and seek personal financial advice from a licensed adviser who has specifically considered your situation. DFRDB scheme rules, tax treatments, life-expectancy factors, and DVA / Centrelink interactions change over time — always confirm current rules and figures with your adviser before any election.

54/11 explained: resign at least two days before turning 55, preserve your CSS benefit, claim it at 55 as a Deferred Benefit. Who can still use it in 2026.

From Age Pension age (67), a redundancy is no longer genuine for tax and the tax-free amount disappears. What older APS members should check before accepting.

Superannuation advice in Canberra — contribution strategy, consolidation, investment options and the CSS, PSS, PSSap and Defence-scheme decisions that make super in this city different.

Missed out on an APS voluntary redundancy, or declined the offer? A specialist guide to retention periods, redeployment, section 29 and what an involuntary package pays.