Personal Insurance Canberra: Specialist Risk-Cover Advice for High-Income Australians

Véurr Financial Planning advises high-income Australians on personal insurance — life, TPD, income protection, and trauma cover. We work with clients across Canberra, Sydney, Melbourne, Brisbane, and remotely. Specialist advice on the structural decisions most peak-earnings households haven’t had a chance to make deliberately.

Véurr Financial Planning advises high-income Australians on personal insurance — life insurance, total and permanent disability (TPD), income protection, and trauma cover. We work with clients across Canberra (our head office is in Deakin), Sydney, Melbourne, Brisbane, Goulburn and surrounds, or remotely.

I’m Maciej Stanek AFP® (ASIC Authorised Representative No. 000449178). My colleague Imran Amjad (ASIC No. 000321135) and I are the advisers you’d work with directly. We specialise in personal insurance structured for households at peak earnings with dependants, mortgages, and lifestyles calibrated to current income — the audience that the standard advice in retail comparison sites is rarely written for. Imran brings specific depth on personal insurance for serving and former Defence Force members, where Defence-specific TPD and income-protection structures interact with DVA entitlements.

Véurr operates as a Corporate Authorised Representative (No. 1307015) of Lifespan Financial Planning Pty Ltd (AFSL 229892). Both Imran and I are listed on ASIC’s Moneysmart Financial Advisers Register — you can verify either of us there before we ever speak.

The Initial Meeting is complimentary — about 45-60 minutes, with no obligation. By the end of it you’ll have a clear sense of whether we’re the right adviser for your situation.

Who we are on personal insurance, and why it sits at the centre of the household plan

Personal insurance is the financial structure that protects a household’s income, debts, and dependants against death, disability, illness, and injury. For households at peak earnings — where the mortgage is sized to current income, dependants rely on continued earning capacity, and lifestyle commitments are calibrated to a full pay packet — getting the personal-insurance program right is the difference between an adverse event becoming a 12-month disruption and a multi-decade financial collapse. The decisions are structural rather than transactional: which of the four cover types you actually need, how much of each, how they are funded (inside super versus outside super), and how they fit together as a single program rather than four bolted-on policies. Specialist advice on this is in-scope under Véurr’s Authorised Representative arrangement.

I (Maciej) have been advising Australian households for over two decades, and personal insurance has been part of every household plan I’ve worked on. Imran and I both consider personal insurance core to the practice, not an add-on. The pattern of clients we see is consistent: most households reaching peak earnings have insufficient insurance for their circumstances — default cover inside their super fund, an employer-paid group policy, sometimes a legacy retail policy from 10-15 years ago, or even a specialist mutual policy for a professional cohort — and have not had any of it reviewed against their current circumstances. The first piece of structural work we usually do for a new client is map what they already have, where the gaps are, and whether what they’re paying for actually matches what they would need at claim.

We’re explicit about who this advice is for: high-income Australians 40+ with dependants, debt, and a 5-25 year runway to a meaningful retirement option. If your situation sits outside that frame, the structural decisions discussed on this page may not apply to you in the same way. Personal insurance is one part of our wider financial planning practice in Canberra — you can also read more about Maciej and Imran.

Maciej, Imran, and how the personal-insurance practice is split

Both advisers at Véurr work across personal insurance, with overlapping but slightly different specialty lanes. Maciej Stanek covers personal-insurance design for the broader high-income Australian household — public servants at EL2 and above, private-sector executives, business owners with buy/sell needs, and professionals (medical, legal, consulting, engineering) whose income shape and underwriting requirements differ from the population at large. Imran Amjad has additional depth on personal insurance for serving and former Defence Force members, where TPD and income-protection structures interact with the Department of Veterans’ Affairs entitlements framework and where condition exclusions on standard retail policies require specific navigation. On day-to-day work, we collaborate across cases. ASIC verifies both of us as Authorised Representatives under Lifespan Financial Planning Pty Ltd, AFSL 229892.

We’re a two-adviser practice — deliberately. When you engage Véurr on personal insurance, you work with one of us directly, and the other is available as a sounding board on specialty matters. We’re not handing files to a paraplanner you’ve never met, and we’re not selling you a product on the first call. The advice work is the work.

Verifiable credentials:

- Maciej Stanek — ASIC No. 000449178. Moneysmart Financial Advisers Register and FAAA Find-a-Planner.

- Imran Amjad — ASIC No. 000321135. Moneysmart Financial Advisers Register and FAAA Find-a-Planner.

- Imran specifically covers the integration between personal insurance and Department of Veterans’ Affairs (DVA) entitlements for Defence members.

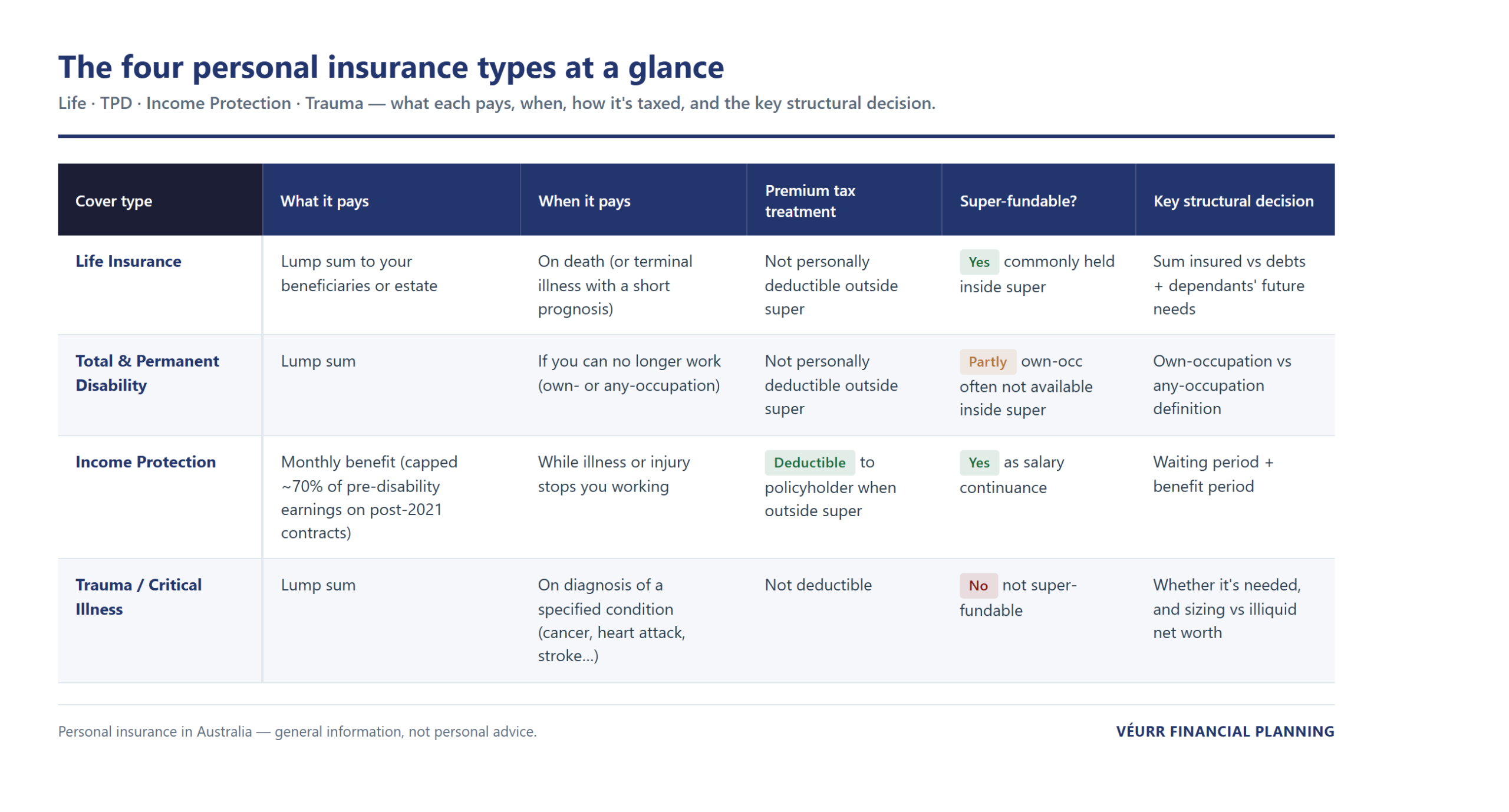

The four personal insurance types in plain English

Personal insurance in Australia is built from four cover types that protect different events. Life Insurance pays a lump sum to your nominated beneficiaries (or estate) on your death or, in some instances, on terminal-illness diagnosis with a short prognosis. Total and Permanent Disability (TPD) pays a lump sum if you become unable to work in your own occupation or in any occupation suited to your training and experience (the definition matters and is the subject of its own structural decision). Income Protection (sometimes also called Salary Continuance) pays a monthly benefit if illness or injury stops you working — generally capped at 70% of pre-disability earnings under the post-October-2021 APRA rules. Trauma or Critical Illness Cover pays a lump sum on the diagnosis of a specified condition (cancer, heart attack, stroke and similar — the schedule of covered conditions varies by policy). Each cover answers a different question; most professional households need a mix, not one of them.

Life Insurance answers the question: “if I die, what does my household need to be financially whole?” The benefit is usually sized against debts to be cleared (mortgage, business loans), dependants’ future living costs, and any specific obligations such as funeral expenses. For most peak-earnings households with dependants and a mortgage, the sum-insured figure sits well above the default cover bundled inside a super fund.

Total and Permanent Disability (TPD) answers a different question: “if I cannot work again, what lump sum does the household need to absorb the change?” The structural decision is the occupation definition — own-occupation (paid if you cannot perform the duties of your specific occupation) or any-occupation (paid only if you cannot perform any occupation suited to your training and experience). Own-occupation is materially more protective and, as a result, generally more expensive. This is its own deep-dive question, which we’ll cover in a forthcoming guide on TPD definitions.

Income Protection answers the question: “if illness or injury stops me earning for months or years, how does the household keep paying its committed outgoings?” The October 2021 APRA reforms reshaped this market — most pre-2021 policies still in force have features (indefinite own-occupation definitions, agreed-value structures) no longer available on new contracts. For peak-earnings households, income protection is usually the largest single line item in the personal-insurance program. We cover this in detail in our Income Protection for High-Income Earners guide.

Trauma / Critical Illness Cover answers the question: “if I’m diagnosed with a serious condition that doesn’t stop me working permanently but may stop me from working for a period of up to two years, what lump sum lets me make the choices I’d want to make?” The benefit can fund a treatment pathway, time off, a change of role, or a financial buffer that the household uses how it sees fit. Less universal than life or TPD or IP — but for households where a meaningful share of net worth is illiquid (business equity, property), trauma cover plays a specific role, often bridging gaps where income protection falls short.

Inside super or outside super — the structural funding decision

Personal insurance can be held inside superannuation (with the super fund as policyholder, premiums deducted from the super balance, benefits subject to superannuation law) or outside superannuation (with the individual as policyholder, premiums paid from after-tax household cash flow, benefits paid directly to the individual or estate), or can be structured by an adviser to get the best of both options — where ownership is with the individual as policyholder, benefits can be more comprehensive than what superannuation law would allow, premiums can be funded by superannuation, and tax deductions can be applied by the super fund on the premiums. The structural defaults differ across the four cover types. Life and TPD are commonly held inside super (premiums non-personally-deductible but funded from pre-tax super contributions, benefit taxation depends on the beneficiary’s status). Income protection premiums are tax-deductible to the policyholder when held outside super, which is the structural starting point for most high-income professional households with cash-flow capacity to fund the premium. Trauma cover is not super-fundable. Most households end up with a deliberately structured hybrid rather than one-or-the-other.

The detail varies meaningfully by cover type. We treat this in depth for income protection specifically in our foundation IP guide; the same structural question applies to life and TPD but with different trade-offs. Tax treatment, benefit pathways, and condition-of-release rules under the Superannuation Industry (Supervision) Act 1993 all shift across the inside-versus-outside choice.

The questions that drive the decision are not just tax. They are:

- Cash-flow capacity. Outside-super premiums are funded from after-tax household income. Inside-super premiums reduce the retirement balance. Neither is free.

- Benefit pathway at claim. Outside-super benefits land directly with the policyholder. Inside-super benefits are subject to condition-of-release rules and may be held in super pending release.

- Cover richness. Some features (e.g. own-occupation TPD definitions, agreed-value income-protection structures, certain trauma definitions) may not be available inside super.

- Estate-planning and beneficiary-nomination requirements. Life insurance held inside super is paid to beneficiaries via the super fund’s beneficiary rules, which differ from the beneficiary rules on outside-super life cover.

This is the structural decision most households we see have never deliberately made — the default cover inside their super fund was activated when they joined the fund, and nothing has been re-examined since. The structured review surfaces what’s actually in place and whether it fits the current household shape.

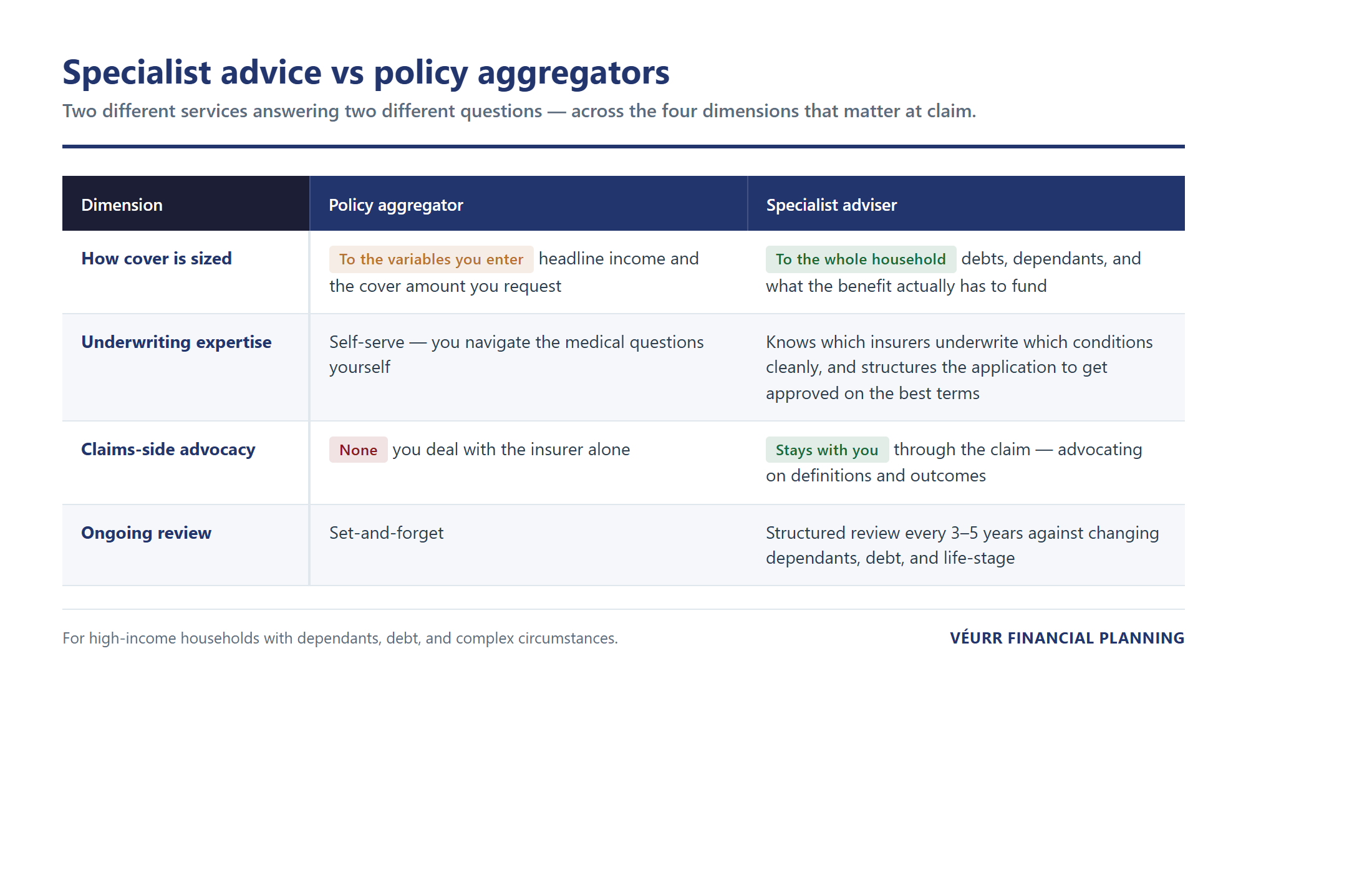

How specialist advice differs from policy aggregators

Specialist personal-insurance advice and the policy-aggregator category (Compare The Market, Canstar, iSelect and similar) are different services answering different questions. Aggregators give you a comparison of headline product features and a price quote for the cover variables you enter — useful if you want the most basic cover, how much of each, how they should be structured, and which features matter at claim. Specialist advice goes upstream of that: working out which cover types you actually need (which is rarely all four at equal weight), sizing each against the specific shape of your household, structuring them across inside-super and outside-super deliberately, and providing claims-side advocacy if and when you ever need to claim. We don’t compete with aggregators — they serve a different market — but we are explicit that for high-income households with dependants, debt, and complex circumstances, the aggregator-only pathway leaves structural decisions on the table.

The difference shows up in four places:

- Sized to circumstances, not just income. A $300,000 earner with two young children, a $1.2m mortgage, and a stay-at-home partner has a fundamentally different cover need from a $300,000 earner with no dependants and no debt. Aggregators ask for income; specialist advice asks about the household’s full financial picture and works backwards from what the policy actually has to fund.

- Underwriting expertise. Specialist advisers know which insurers underwrite which conditions cleanly, which require detailed medical loadings, and which to avoid for specific occupations. For professionals (medical, legal, consulting, business owners), the underwriting pathway often determines whether the cover gets approved at all — and on what terms.

- Claims-side advocacy. If you ever need to claim, the difference between a smooth payout and a contested claim often comes down to how the original application was structured, whether the definitions in the contract actually fit the medical event, and whether the claimant has someone in their corner navigating the insurer. Specialist advisers stay with clients through the claim.

- Ongoing review. A personal-insurance program written when you were 38 with a $600,000 mortgage and two kids is not the right program at 52 with the mortgage half-paid and the kids leaving home. The structural review point — every 3-5 years for most households — is where specialist advice differentiates from the set-and-forget aggregator pathway.

Questions to ask before engaging any adviser.

The four design levers — a brief framing

Every personal-insurance policy is built from four design levers that, together, shape what you pay and what you receive at claim. Cover amount is the sum-insured (life, TPD, trauma) or monthly benefit (income protection) — sized against debts, dependants’ needs, and committed outgoings rather than headline income alone. Waiting period (income protection only) is the time between the disability starting and the benefit payments beginning — longer waits cost less but require deeper household emergency reserves. Benefit period (income protection only) is how long the benefit will be paid — to age 65, or a fixed two-year cap, with significant cost differences between them. Ancillary benefits include guaranteed renewability, indexation, partial-disability provisions, rehabilitation support, and similar features that affect cover quality but rarely headline pricing.

We go deep on these levers — specifically for income protection — in the foundation IP guide. The same lever-framing applies across life, TPD, and trauma with adjustments specific to each cover type. The structural starting point for any household is to choose the levers deliberately, with sight of the household’s full circumstances, rather than accepting the defaults bundled into a policy from a comparison site.

Tax treatment of personal insurance — premiums and benefits

Tax treatment of personal-insurance premiums and benefits depends on the cover type, the structure (inside-super versus outside-super), and the policyholder’s circumstances. Income protection premiums paid from after-tax household cash flow on a policy held outside superannuation are generally tax-deductible to the policyholder. Life and TPD premiums paid outside super are generally not personally tax-deductible. Premiums on policies held inside super are funded from the super account balance and are not separately tax-deductible to the member. Benefits at claim are taxed differently across cover types and structures: income protection benefits paid outside super are generally assessable income at marginal rates; life-insurance lump sums paid to dependants are generally tax-free; TPD benefits paid from super are taxable in part depending on the recipient’s age and components. Personal tax outcomes always depend on individual circumstances — this is general information, not personal tax advice.

For specific tax detail, the Australian Taxation Office (ATO) maintains current guidance on income-protection premium deductibility, and your accountant should be involved in any structural decision that depends on a specific tax outcome. We don’t run the tax calc — we work with the after-tax outcome of the cover decisions you’re considering.

How we work — your first meeting and beyond

The advice process is the same regardless of which cover types you ultimately need: five steps, no surprises. The personal-insurance-specific element is that the strategy work usually starts by mapping your existing cover from all sources — default cover inside your super fund, any employer group policy, any standalone retail or mutual policy — and then identifying the gap to the structurally appropriate level. Most households we see find that the audit alone clarifies several decisions.

Step 1 — Initial Meeting (complimentary, 45-60 minutes). This is a conversation, not a sales meeting. You tell us what’s on your mind. We tell you what we’d typically look at for someone in your situation. By the end of it, you’ll know what advice would actually involve, roughly what it would cost, and whether we’re the right adviser to deliver it. There’s no obligation to proceed.

Step 2 — Engagement decision. Both sides decide. If we’re not the right fit, we’ll say so and refer you elsewhere where we can. If we are the right fit, we complete a fact find document covering scope, fees, and timelines.

Step 3 — Discovery and strategy development. We gather what we need to advise properly — your existing insurance schedules from all sources, super fund statements, payslips, tax positions, the household’s debt and dependants’ position. Then we map what’s in place against what’s needed and model the structural alternatives.

Step 4 — Statement of Advice (SoA). Once the strategy work is complete, we prepare a written Statement of Advice — the regulated document setting out our recommendations and the reasoning. We walk through it together so you fully understand each recommendation before any decisions are made.

Step 5 — Implementation and ongoing review. For clients who continue with us, we coordinate implementation and meet annually (more often if circumstances change) to review the program against where you actually are. Personal-insurance programs need periodic review against changing dependants, debt, income, and life-stage — the review point is part of the structural design.

Common mistakes we see in professional households

The most common mistake we see in professional households is complacency. Clients’ reasoning is that personal insurance is not required as they are healthy and/or have a safe, stable job. But the point of insurance is to protect the insured from an “unforeseen” or “unexpected” event. The risk is transferred from the insured to the insurer when a client pays the premium. The pricing of the premium is based on the insurer’s claims history for that event, so if the premium is deemed high by the insured, this means the risk of the insurance event occurring is actually higher than the individual assumes it to be. I tell all my clients that I hope they will never claim on their policy, and for most of my clients this is the case. For those who are actually in the unfortunate situation where the insurance event occurs, being insured is the difference between losing a significant amount of their accumulated lifelong wealth and making sure that their long-term financial planning needs are met.

The second common mistake is reviewing insurance but leaving the implementation to a later date. In many instances a person’s health deteriorates over time. What would have been a very comprehensive policy in the initial review, with no loadings or exclusions, can become significantly more expensive and less comprehensive as someone’s medical history becomes longer. These clients would have been much better off even insuring part of their needs when they are young and healthy, and increasing the cover at a later date at what may be less favourable terms. Deterioration of health leads to claims; no one is worried about claims when they are fit and healthy.

The third common mistake is the belief that “my super fund and/or employer will protect me”. In my experience, neither of these entities is structured to look after your individual best interests — they are following regulations and meeting their own obligations. I have seen instances where a client lost an arm and a leg in a car accident, which led the employer to let her go from her job as a Registered Nurse. Even though it was obvious that the client was Totally and Permanently Disabled (under the age of 30) and would never be able to work in her profession again, the super fund’s Total and Permanent Disability cover denied her claim — because she was still capable of making a phone call and therefore, in the insurer’s view, could find work in a call centre.

Common questions we hear from prospective clients

What’s the difference between life insurance, TPD, income protection, and trauma cover?

Life insurance pays a lump sum on death (and usually terminal illness with a short prognosis). TPD pays a lump sum if you become unable to work — either in your own occupation or any occupation, depending on the policy definition. Income protection pays a monthly benefit if illness or injury stops you earning. Trauma cover pays a lump sum on diagnosis of a specified serious condition. Each answers a different question. Most professional households need a mix — not one of them alone, and rarely all four at equal weight.

Do I need personal insurance if I have default cover in my super?

Default cover inside super is a starting point, not a complete program. For most peak-earnings households we see, the default cover sits well below the structurally appropriate level — modest sums for life and TPD, no trauma cover or income protection at all. Default cover also doesn’t pay attention to who you are; it’s sized to a population, not your household. A structured review compares what’s in place to what would actually be needed at claim.

How much cover do I actually need at $175k+ income?

There’s no single dollar number that’s right for every $175k+ household. The cover-sizing question depends on dependants, debt (especially mortgage), the household’s other resources, and how the household’s lifestyle is calibrated to current income. We size cover against what the benefit actually has to fund — committed outgoings during a claim, debts to be cleared at death, household reconfiguration costs after TPD — not against headline income alone. The income figure is one input, not the answer.

Are personal insurance premiums tax-deductible?

It depends. Income protection premiums paid from after-tax household cash flow on a policy held outside superannuation are generally tax-deductible to the policyholder. Life and TPD premiums paid outside super are generally not personally tax-deductible. Premiums on policies held inside super are funded from the super account balance and are not separately deductible to the member. Tax outcomes always depend on personal circumstances — confirm specifics with your accountant.

What’s the difference between own-occupation and any-occupation TPD?

Own-occupation TPD pays if you cannot perform the duties of your specific occupation (e.g. a surgeon who can no longer operate). Any-occupation TPD pays only if you cannot perform any occupation suited to your training and experience and/or daily duties like showering or making a sandwich. Own-occupation is materially more protective for high-skill specialists, which means it can be more expensive. On income protection specifically, new contracts issued since the October 2021 APRA reforms typically apply an own-occupation definition only for the first two years of a claim, then move to an any-occupation test; TPD has its own definition framework separate from that income-protection rule. The choice is one of the largest structural decisions on the TPD line.

How does personal insurance work for business owners?

Business owners typically need a more carefully designed personal-insurance program because the income definition is more complex (salary plus the business profits attributed to their work), pre-disability earnings are harder to demonstrate to an underwriter, and the business itself may need separate cover (key-person insurance, business-expenses cover, buy/sell agreement funding) that complements the personal cover. We work across the personal and business insurance lines as a coordinated piece rather than as separate policies bolted together.

What if I have a pre-existing condition?

A pre-existing condition doesn’t automatically rule out cover — but it changes the underwriting pathway. Insurers may apply specific exclusions, premium loadings, or in some cases decline new cover. The specialist-advice value-add is knowing which insurers underwrite specific conditions cleanly and which to avoid for your situation, structuring the application to give the cleanest possible outcome, and where new cover isn’t available, preserving any existing cover that may already be in place under more favourable terms.

How do I verify Véurr’s credentials independently?

ASIC’s Moneysmart Financial Advisers Register lists both Maciej Stanek (000449178) and Imran Amjad (000321135) with our authorising AFSL (Lifespan Financial Planning Pty Ltd, AFSL 229892) and compliance history. The FAAA Find-a-Planner directory also lists both of us as members. We recommend you check us — and any adviser you’re considering — on both registers before engaging. It takes a minute.

Verify our credentials independently

We’re easy to verify. The federal government maintains the Moneysmart Financial Advisers Register at moneysmart.gov.au as the authoritative source on who’s authorised to provide financial advice in Australia and what their compliance history is.

- Maciej Stanek — ASIC Authorised Representative No. 000449178. Verifiable at the Moneysmart Financial Advisers Register and the FAAA Find-a-Planner directory.

- Imran Amjad — ASIC Authorised Representative No. 000321135. Verifiable at the Moneysmart Financial Advisers Register and the FAAA Find-a-Planner directory.

- Lifespan Financial Planning Pty Ltd — Australian Financial Services Licence No. 229892. Verifiable on ASIC’s professional registers (AFSL search).

- Véurr Financial Planning Pty Ltd — Corporate Authorised Representative No. 1307015 of Lifespan Financial Planning. ABN 16 635 751 423.

Before you engage any adviser — us included — we suggest checking the Moneysmart register yourself. It takes about a minute.

Book your complimentary Initial Meeting

Our head office is at Suite 30, 2 King Street, Deakin ACT 2600. We see clients in person there, in Sydney, Melbourne, Brisbane, and Goulburn and surrounds by arrangement, or remotely.

The Initial Meeting is complimentary and runs about 45-60 minutes. You’ll come away with a clear view of whether personal-insurance advice would help your situation, what it would involve, and whether Véurr is the right firm to deliver it. No obligation, no follow-up sales call.

Véurr Financial Planning Pty Ltd (ABN 16 635 751 423) is a Corporate Authorised Representative (No. 1307015) of Lifespan Financial Planning Pty Ltd (ABN 23 065 921 735, AFSL 229892). The information on this page is general in nature and has not been prepared with regard to any individual’s objectives, financial situation, or needs. Before acting on any general information, consider its appropriateness having regard to your own objectives, financial situation, and needs, and obtain the relevant Product Disclosure Statement before making any decision about a financial product.